I-Bonds Fall Back to Earth

U.S. government I-Bonds are about to be deposed as the undisputed king of the fixed-income hill.

Two years ago, I-Bond rates began an inflation-driven upward move that eventually (in May 2022) hit an annualized 9.62%(!) — a remarkable return for a virtually risk-free investment. Since November, the annualized rate has stood at a still-strong 6.89%.

But with inflation cooling (somewhat), I-Bonds are falling back to earth. The new I-Bond rate, to be announced May 1, won't be quite so attractive.

From MarketWatch:I-bonds are priced based on two factors: a variable rate based on six months of inflation data (from October through March) and a fixed rate that is less transparently calculated. The latest CPI numbers for March indicate that the variable rate is going to pan out at an annualized rate of 3.38%....However, not all I-Bonds will experience a rate change on May 1. Any I-Bond purchased before the end of April will earn the current 6.89% annualized rate for the next six months. After that, such bonds will reset (for the next six months) to the new less-than-4% annualized rate. [MAY 1 UPDATE: Much to the surprise of I-Bond observers, the May 2023 rate is 4.30%, which includes a 0.9% fixed rate.] I-Bond Rates Are Announced Each May and NovemberThe current fixed rate is 0.4%, and it’s still unclear what the next one will be, but it’s unlikely to stray too far from that threshold.

If the composite annualized I-bond rate stays in line with predictions, it will come in [around 3.79%], making I-bonds less lucrative in the short-term than other comparable investments like Treasury bills, TIPS, CDs and even some high-interest savings accounts.

May 2023

- 3.79% (projected, not yet official)

- 4.30% (incl. fixed rate of 0.9%)

Nov 2022

- 6.89% (incl. fixed rate of 0.4%)

May 2022

- 9.62% (fixed rate was 0.0%)

Nov 2021

- 7.12% (fixed rate was 0.0%)

May 2021

- 3.54% (fixed rate was 0.0%)

Nov 2020

- 1.68% (fixed rate was 0.0%)

May 2020

- 1.06% (fixed rate was 0.0%)

Running the numbers

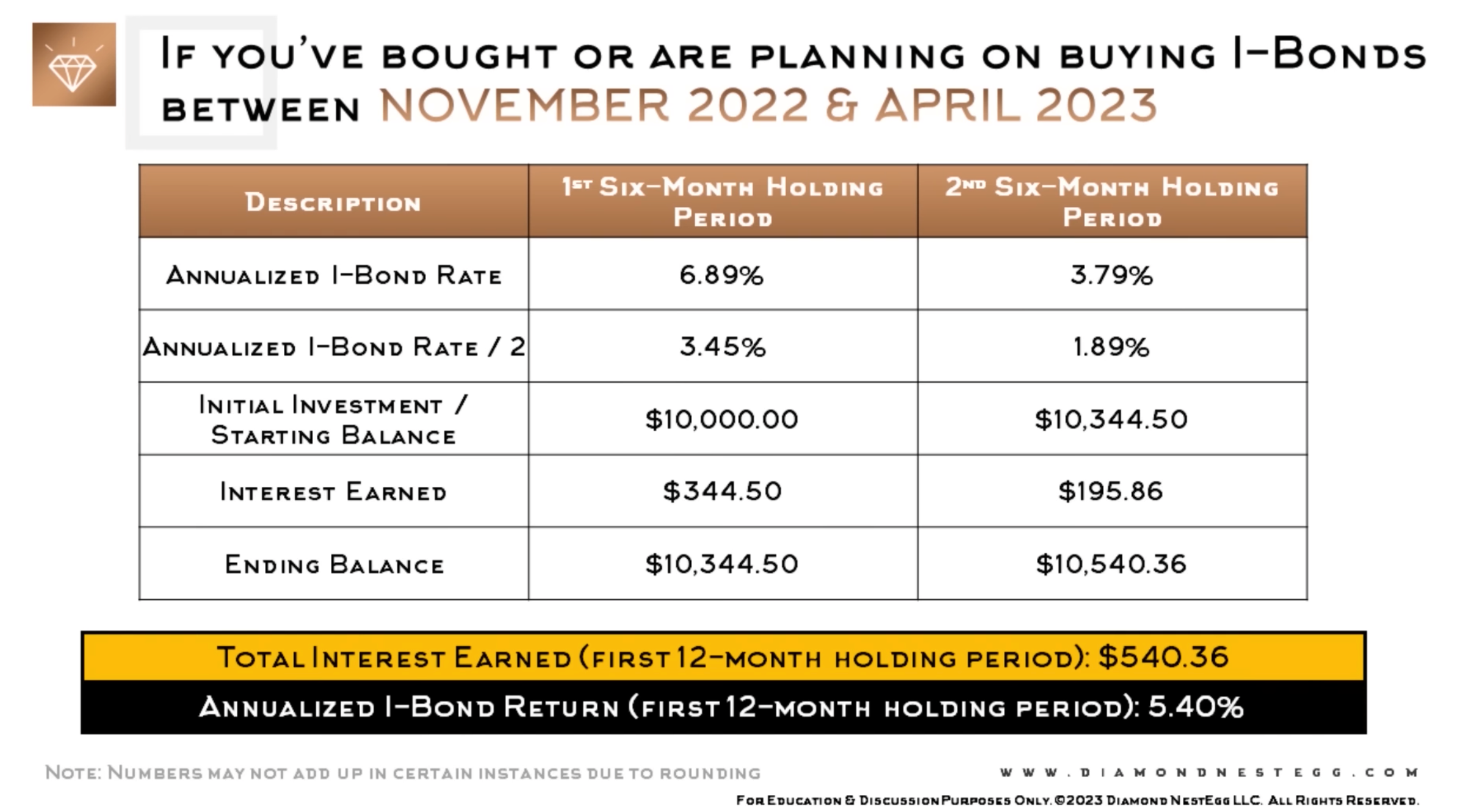

Because annualized rates are in effect only for six months (yeah, that's confusing), an annualized rate must be divided by two to calculate the rate earned over a semi-annual period.

YouTuber Jennifer Lammer, a self-described "super saver," created a helpful graphic that shows how the current rate (6.89%) and the expected rate (3.79%) would result in a one-year dollar gain of more than $500 on a $10,000 investment. As you can see, $10,000 invested now in an I-Bond would grow to $10,540.36 over 12 months — a return of 5.40%. That's not bad, but it won't make anyone enthusiastic at a time when some CDs are paying that much and without the restrictions that I-Bonds carry (see below).

As you can see, $10,000 invested now in an I-Bond would grow to $10,540.36 over 12 months — a return of 5.40%. That's not bad, but it won't make anyone enthusiastic at a time when some CDs are paying that much and without the restrictions that I-Bonds carry (see below).

That said, if you've already invested in I-Bonds, or plan to purchase some between now and the end of April, you'll still earn a decent return — and remember that I-Bonds are virtually risk-free. Further, depending on the course of inflation over the next six months, the rate could tick up again.

If you want to run your own I-Bond calculations, check out this specialized online calculator.I-Bond restrictions

- Direct purchase only. You can't buy I-Bonds within your retirement or brokerage account. You must open an account at Treasury Direct. However, the process isn't too painful, and the purchase money transfers from your bank account.

**

Related Articles

May 25, 2025

How To Choose The Right Financial Advisor

For Christians who want their finances to reflect their faith, it’s about more than just numbers and returns....

April 13, 2025

Time for Foreign Stocks to Shine?

Have stocks shifted in a different Direction? Recent pickup in foreign returns has certainly grabbed our attention....

March 18, 2025