Inflation-Adjusted Tax Provisions May Boost Your 2023 Take-Home Pay

Inflation has at least one upside: higher inflation can reduce your tax liability.

Inflation has at least one upside: higher inflation can reduce your tax liability. That’s because many tax provisions in the U.S. are indexed to inflation. As inflation rises, tax thresholds move upward, resulting in tax brackets, deductions, and limits that are more taxpayer-friendly — and that’s exactly what’s on tap for 2023.

Bracket shifts

- Income Tax

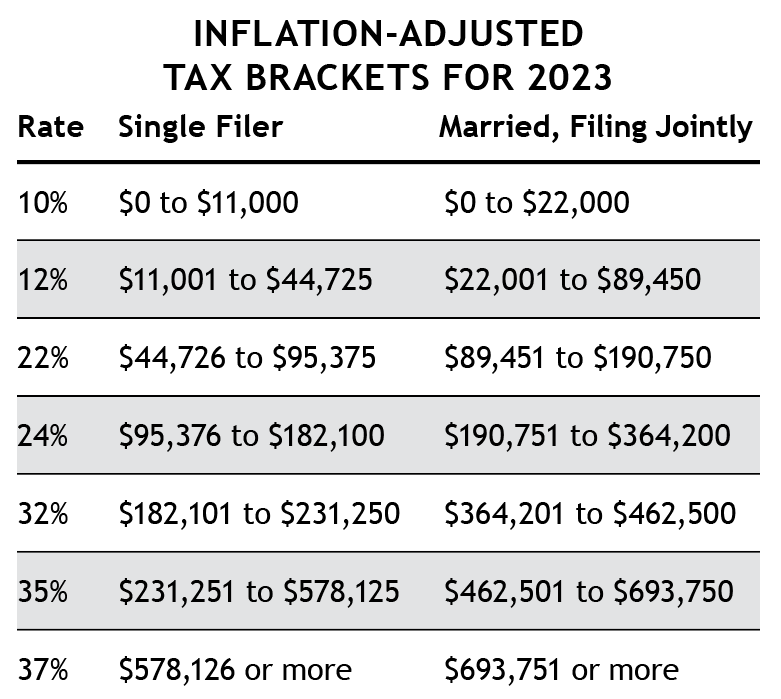

Under federal tax law, income isn’t taxed at a single rate. Instead, the U.S. tax system has seven rates, each applying to a different level of taxable personal or household income. (Bear in mind, of course, that any tax filer can reduce taxable income to some degree via various credits and deductions.)

The first income range is taxed at 10%, and the next at 12%. Then some at 22%, 24%, 32%, and 35%. The highest earners face the top tax rate: 37%.

The income thresholds at which each tax rate begins and ends are set by law, but those thresholds are adjusted each year to account for inflation. The annual adjustments keep taxpayers from being pushed into higher brackets by income increases that aren’t true gains but are merely designed to keep pace with rising overall costs.

In most years, the tweaking of tax-bracket thresholds is minor. Not so for 2023. Because of strong inflation, the starting and ending points for most tax brackets have been revised upward significantly —by about 7%. (The first bracket always begins at $0, and the top bracket is always open-ended.) The 2023 dollar ranges for the seven brackets are shown in the table at right.

The bracket adjustments mean some income will be taxed at a lower rate in the new year than the same amount would have faced if earned in 2022. In turn, most workers will see slightly higher take-home pay starting in January because the IRS must adjust its tax-withholding formula to account for the updated bracket ranges.The impact of the inflation adjustments is most significant for those whose incomes cross multiple thresholds, especially earners whose income falls near one of the changeover thresholds — i.e., where one bracket gives way to another.

Suppose, for example, a taxpayer has a taxable household income of $89,000 in 2022 and expects the same for next year.

For the 2022 tax year, any income above $83,550 is taxed at 22% (married, filing jointly). But in 2023, because of the inflation adjustment, the 22% bracket won’t begin until income reaches $89,451. So, in this example, roughly $5,500 in income that faced a 22% rate in 2022 would be taxed at only 12% in 2023. That translates to a tax savings of about $550.The progressive nature of the tax brackets — i.e., higher earners pay higher rates — means the greatest tax benefits from the bracket shifts will flow to those in the upper-income ranges. For tax year 2022, for example, a married couple filing jointly faces the 32% rate starting at $340,101 of income. In 2023, however, the 32% bracket won’t kick in until household income reaches $364,201.

That means a hypothetical couple with taxable income of $360,000 in 2022 and again in 2023 would pay $1,500 less in income taxes in the second year (assuming no other change in their overall tax picture).

- Capital-Gains Tax

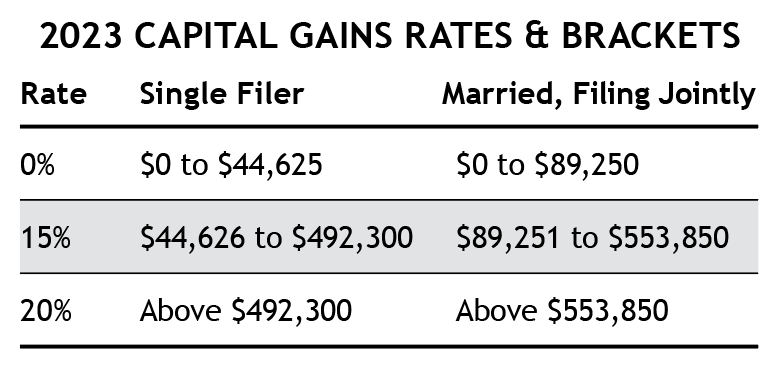

Income brackets for long-term capital gains taxes are shifting upward by about 7% as well. Capital gains rates are applied against assets sold after being held for more than one year.

Larger standard deductions

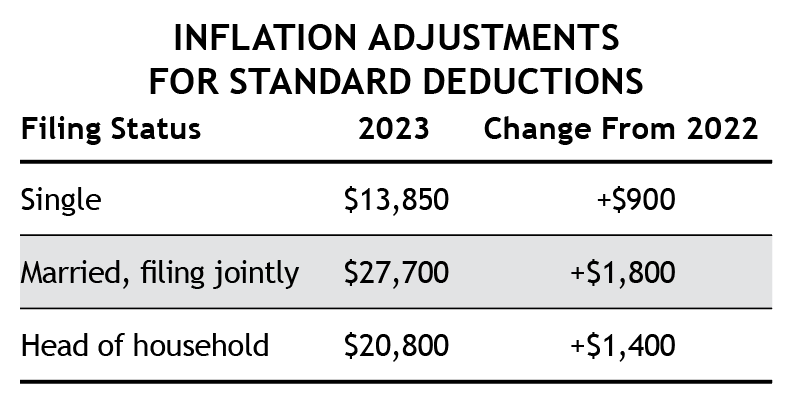

Besides the inflation-driven bracket shifts, many taxpayers will face reduced tax obligations in 2023 for another reason: “Standard deductions” are being adjusted significantly too, as shown in the table below. (A standard deduction is the amount of income a taxpayer may automatically shield from taxation. Nearly 90% of taxpayers claim the standard deduction. Other taxpayers “itemize,” opting to claim various specific deductions allowed by law.)

Standard deductions for tax filers over age 64 are even greater than the amounts shown in the table. Married couples filing jointly can claim an additional $1,500 deduction per person (if 65 or older). That’s up from $1,400 in 2022. For senior-age single filers, the additional deduction is $1,850, up from $1,750 for the current tax year.

Rising ceilings

In all, inflation adjustments will alter more than 60 tax provisions for tax year 2023. Here are a few more of them:

- Retirement Account Limits

The annual amount an employee can contribute to a 401(k) or a similar workplace retirement account will rise to $22,500, up from $20,500 this year. Employees ages 50 and up can make “catch-up” contributions of an additional $7,500, up from $6,500 in 2022.

For IRAs, the annual contribution amount will rise to $6,500 (up from $6,000). Unfortunately, catch-up IRA contributions (for those 50 and up) remain capped at $1,000 because that limit is not indexed to inflation.

- Flexible Spending Accounts

FSAs allow employees to contribute pre-tax dollars into a personal account that is then used to pay qualified medical expenses. For 2023, the annual allowed contribution will rise to $3,050, up from $2,850 in 2022.

- Health Savings Accounts

HSAs are tax-advantaged accounts available only to people with high-deductible health plans. The limit for pretax contributions to an HSA will increase in 2023 to $3,850 for individuals (up from $3,650). For a family, the new limit is $7,750 (up from $7,300). HSA holders over age 54 but not yet eligible for Medicare can make an extra $1,000 "catch-up" contribution.

- Non-Taxable Gifts

In tax year 2023, you’ll be able to make a gift — of cash, stocks, property, etc. — of up to $17,000 to any person, or even multiple people, without incurring any gift-tax liability. (The limit for 2022 is $16,000.) If you’re married, each spouse can make gifts of up to $17,000.

The lifetime exclusion is rising too. The amount you can give during your lifetime (or at death) and avoid federal estate and gift taxes is rising from $12.06 million to $12.92 million.

Remaining the same

Not all tax thresholds and ceilings are indexed to inflation so some items won’t change. Among them:

- Child Tax Credit

The credit will remain at $2,000 per child under the age of 17. (The credit was increased temporarily in 2021 but reverted to $2,000 in 2022.)

- Investment surtax

The income thresholds for the 3.8% net investment surtax remain unchanged for 2023: $250,000 for married couples filing jointly and $200,000 for singles.

Other considerations

Because inflation adjustments may lead to lower federal tax obligations in 2023, you may want to delay some 2022 income until next year if possible. For example, you could ask your employer to delay any end-of-year bonus until January.

Also, bear in mind that the tax laws of your state may not require inflation adjustments. So it’s possible, depending on where you live, that while your federal obligation could decline in 2023, your state tax obligation (if any) could increase.

*Image used with permission. * *Image used with permission. * *Image used with permission. * *Image used with permission. *Related Articles

November 17, 2024

How Women Will Lead the Great Wealth Transfer

Women are set to inherit the majority of the wealth in the Great Wealth Transfer from Boomers--here's the opportunity....

October 25, 2024

Reverse Mortgages: A closer look at non-recourse protection

There may not be a greater safeguard in consumer protections than the non-recourse clause....

August 31, 2024

A Christian View of Work

Christians often fall into the trap of thinking that work is punishment, but that is a worldly view and not biblical....